There’s a quote from Lauren Lavin, executive director, commerce practice lead at Group M that sums up the state of retail media better than any white paper:

“They sort of write their own rules as far as how they’re going to run their media. And then they grade their own homework and hand it back to you as performance metrics.”

One reports on a 60-day attribution window, another uses a 30-day window and a different ROAS calculation, and a third measures incrementality in a way you cannot replicate or audit. Every network looks great in its own dashboard. But none of them compare apples to apples, which means you can’t tell where your next dollar should go.

You also are only targeting people who buy from that retailer (or, in the case of off-site display, retailers adjacent to them). You don’t know who else you’re missing out on.

Independent commerce media networks, like Kard, aren’t tied to a single retailer. They use first-party transaction data from across many retailers, banks, and fintechs to connect brands with verified buyers — rather than locking you into a single company’s ecosystem.

Here’s how the two differ, when to go with an independent commerce media network, and what to look for in a vendor.

What’s the Difference Between an Independent Commerce Media Network and Walled Gardens?

Before we get too deep into the differences, let’s define commerce media.

Commerce media is a form of digital advertising that reaches consumers in environments where they’re actively shopping, checking out, or transacting. There are two types of commerce media:

1. A Walled Garden Network

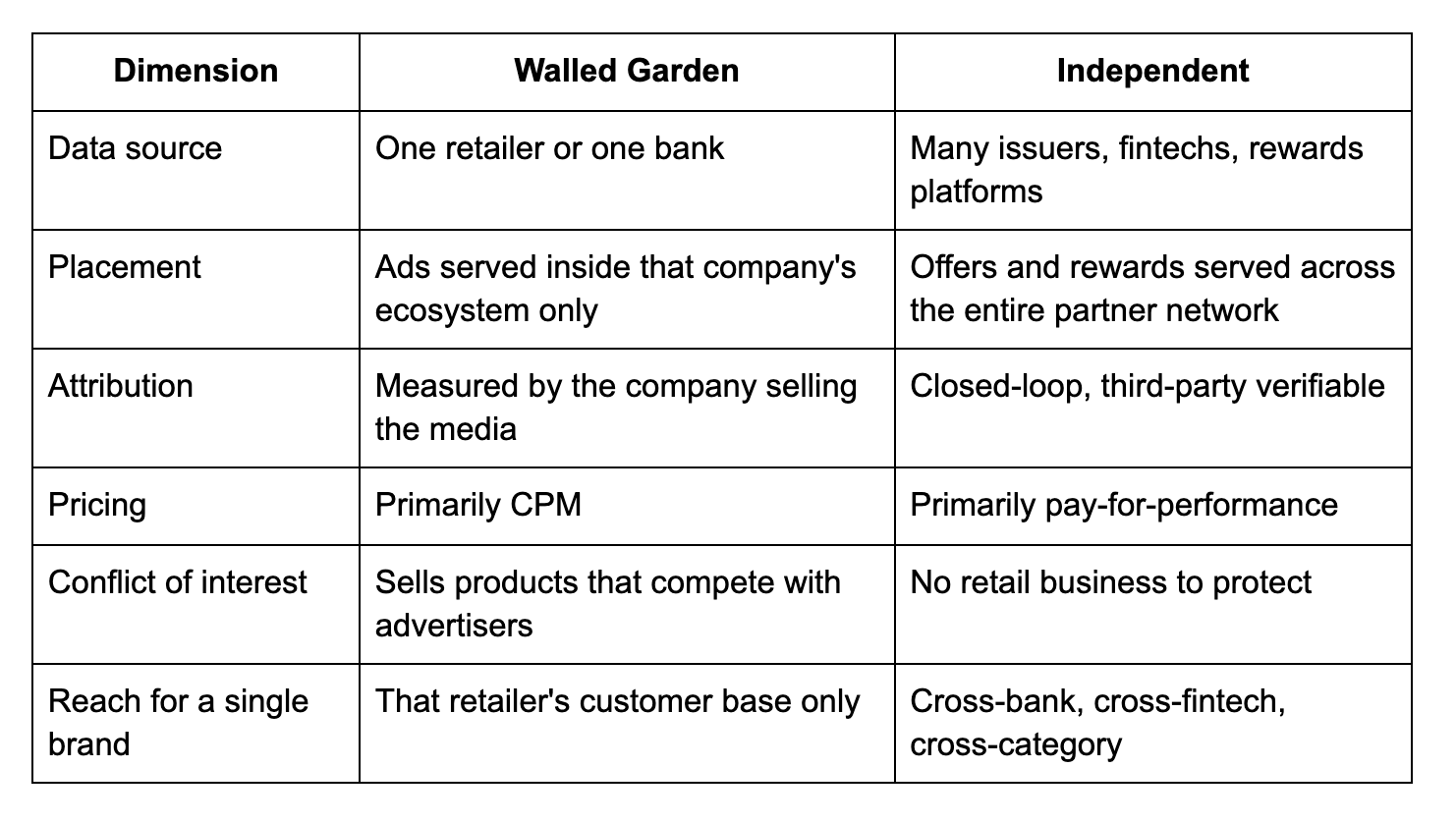

These are run by one retailer or one bank, using its own first-party customer data.

Brands buy placements through the company’s self-serve ad platform (or through a managed-service team for larger budgets), choose audience segments built from that retailer’s purchase history, and then run ads on the company's surfaces — aka its website, its app, on in-store screens, and off-site display through the retailer's DSP.

Measurement happens inside the same platform, and pricing is usually CPM or auction-based. Some examples are: Amazon Ads, Walmart Connect, Kroger Precision Marketing, Chase Media Solutions, and Mastercard Commerce Media.

These networks are a major part of the shift marketers are making toward performance-driven, outcome-based media, but they’re just one piece of the puzzle (more on that later).

2. An Independent Commerce Media Network

Instead of relying on one company’s first-party data, independent commerce media networks pull transaction data from multiple fintechs, FIs, and rewards platforms. Brands then pay to serve up relevant offers to cardholders across the network’s partner apps.

Because the network sits across so many partners, that means a single campaign can reach the same person whether they’re swiping their BankMobile Vibe card at Bombas checkout or their Atlas card at their local gas station.

Pricing is usually pay-for-performance, meaning you pay only when a verified purchase happens (not for impressions).

Walled Garden vs. Independent Commerce Media at a Glance

Walled Gardens are Showing Cracks

The conditions that made walled gardens work in 2020 are the same ones making them harder to defend in 2026.

Big retailers had the first usable purchase data at scale, so they built ad businesses on top of it. Makes sense.

But now that advantage is capped. Sure, these companies are still going to gain more loyal fans, and yes, most of them will still be a part of your target audience. What walled gardens can’t give you is the rest of the picture:

- Where do those customers shop when they’re not at a big box store?

- What do they buy?

- Who isn’t shopping there that you want to get in front of?

Limited Reach

A campaign on Walmart Connect reaches Walmart shoppers buying on Walmart. That is a real audience and it converts. But it is also just one customer base.

A CPG brand might sit on shelves at Walmart, Target, Kroger, Whole Foods, and three other DTC marketplaces. Running on Walmart’s network alone tells you nothing about the customer who saw your Walmart ad and then bought your product at Target.

For categories where customers shop omnichannel (most categories now) that is a hard ceiling.

Conflicts of Interest

Retailers running these media networks sell their own competing products. Amazon sells Amazon Basics. Walmart has Great Value basics. Target pushes Up & Up. Which means it’s not a neutral auction. One anonymous, frustrated marketer quoted in Digiday suggests:

“We should firewall the merchant from all media conversations entirely. The incentive structure for this whole thing is goofed.”

Banks running commerce media have a different flavor of this. Chase Media Solutions, for example, advertises only to Chase cardholders. That is a high-income, high-credit-tier audience, but it is just one slice of the country. The data is rich (pun intended) and biased at the same time.

Fragmented Spend and Measurement

You can’t just work with one retail media network anymore, because that won’t saturate the market enough. That means most brands are running on five, six, sometimes ten walled gardens at the same time. Each one with its own metrics, attribution model, and definition of incrementality.

Without a bunch of pivot tables or asking AI for help, you’re not quite sure what’s performing best where. And building a consolidated view of the customer is an internal data engineering project most brands don't have the budget for.

Independent Commerce Media Networks Fix These Problems By Design

They’ve got:

Cross-Retailer, Cross-Category Reach

Independent networks aggregate transaction data across many partners. One campaign can reach a customer regardless of which card they swipe or which retailer they walk into.

This matters most for the audience marketers are working hardest to reach. Gen Z and Millennials hold one to two cards each, use multiple rewards apps, and shop across categories in the same week. Reaching them through any single retailer's network captures a fraction of their wallet.

Did you know? Kard has over 47M cardholders in Kard’s network who buy at hundreds of different merchants. That breadth gives marketers a 360-degree view of their customers’ shopping patterns, and lets them send hyperpersonalized cash back offers based on billions of dollars-worth of transaction data from all kinds of credit card, debit card, and fintech platforms — including Buy Now Pay Later apps, which had a 9% YoY increase in volume this year.

Neutral Measurement

An independent network doesn't sell the products being advertised. There's no house brand competing with you on the shelf, no incentive to massage attribution in the network's favor.

Attribution is closed-loop and tied to verified online and in-store transactions across the partner network, which means the same methodology applies, whether someone bought online or in-store, using their credit card, debit card, or a BNPL plan. The math is the math.

Read more about how to measure incremental lift.

Pay-for-Performance Model

Most walled gardens charge by CPM, sponsored placements, or auction-based search. Brands pay for impressions or clicks and hope conversion follows.

The dominant independent model is pay-for-performance: the brand pays when a verified purchase happens. This is a totally different risk profile, a different budget conversation internally, and yields different, clearer, conversion-oriented results.

Where Independent Networks Fit in Your Media Mix

Right off the bat, we want to say: independent commerce media is not a replacement for walled gardens in every situation.

A brand that sells exclusively through Amazon should obviously run on Amazon's network. The argument here is for the much larger group of brands that sell across many channels. That want to:

- Scale new customer acquisition in categories one retailer cannot reach

- Remind former customers about their brand in new ways (like their banking app)

- Use incrementality testing as a check on closed-network attribution

- Reach demographics that shop outside of big box retailers (like Gen Z or Millennials)

- Capture the same customer in multiple contexts across a billing cycle

As third-party cookies disappear and marketers face growing pressure to prove ROI, independent commerce media expands your reach and ties ad exposure directly to measurable outcomes.

- It reaches people who are ready to buy — people who are actively browsing, booking, or checking out.

- It uses real, verified commerce data. Discounts, promos, and rewards are surfaced based on consumers’ actual purchase behavior.

- It’s measurable by design. Because sponsored ads run in closed-loop ecosystems, you can track spend to sales, including lift, loyalty impact, and even SKU-level detail.

What to Look For in an Independent Commerce Media Partner

The category includes several networks, not all built the same way. Six criteria worth pressing on before signing:

- Network breadth. How many issuers, fintechs, and rewards platforms are in the network, and what demographics do they cover?

- Exclusive issuer relationships, so the same customer is not seeing the same offer through three competing networks.

- Closed-loop attribution covering both online and in-store purchases.

- Pay-for-performance pricing, not CPM dressed up in new language.

- Granular segmentation for new, repeat, and lapsed customers.

- Reporting on true incrementality, not last-click conversion.

Platforms like Kard are already giving merchants a scalable channel to engage consumers and link brand exposure directly to verified online and in-store purchases.

Curious what we can do for you? Book a demo to see what 47M cardholders across hundreds of merchants can do for your next campaign.