Most growth teams are running “multichannel” - pushing spend across Google, Meta, and programmatic - without fixing the core leaks: audience overlap, siloed data, and skyrocketing CPA.

This guide breaks down the true difference between omnichannel and multichannel marketing, and why financial-app rewards outperform traditional channels on cost, data, and incremental sales. Here’s how to future-proof your marketing plan.

The current state of multichannel advertising: where budgets leak

Bot traffic Is consuming real budgets

Nearly 40% of digital ad budgets are lost to bot traffic. These invalid clicks never convert, but still drain spend and distort performance metrics. Every bot click means less budget for real buyers, lowering actual returns and inflating reported reach. Most display platforms are unable to filter this traffic out, leaving media buyers with inflated impression counts and weak post-click performance.

Programmatic channels are especially exposed. Fraudsters deploy sophisticated bots that mimic human behavior, making detection harder for legacy DSPs. Despite promised protections, automated filters routinely miss click farms and invalid traffic sources. For marketers, this means budget is wasted on non-human impressions, while genuine acquisition costs spike.

Industry data and analysis from leading LinkedIn voices reveal that bot traffic can quietly consume up to 40% of campaign budgets, and in some verticals, the number is even higher. This is a primary reason why ROAS in programmatic often trails behind direct channels and why ad fraud prevention has become a top priority for performance teams.

Platforms that rely on transaction-backed data, such as card-linked offer networks, eliminate this waste. Every interaction is tied directly to verified spend, not a questionable click - ensuring every dollar is working toward actual conversion.

Ad costs keep climbing across major platforms

CPC inflation is squeezing merchant margins. Across Google, Meta, and other major ad platforms, average CPCs have risen 15–20% year-over-year since 2024. In some categories, search keywords now exceed $50 per click, making customer acquisition through paid search unsustainable for most brands. For social, CPMs are climbing even faster than conversion rates, forcing advertisers to pay more for less qualified traffic.

The bottom line: rising ad costs mean less room to optimize for profit. Marketing teams that once justified spend with steady CPA are now seeing their budgets eroded by inflation with no improvement in conversion volume. Advertising budget optimization is harder than ever when every channel competes for the same audience - often with duplicated spend and diminishing returns.

Broken attribution in walled gardens

Attribution challenges are mounting as walled gardens clamp down on data sharing. After iOS 14.5, multi-touch visibility dropped by 35%, leaving marketers with fragmented, incomplete customer journeys. Cookie deprecation has only made cross-platform attribution more elusive.

Data silos block unified customer views, forcing teams to optimize channel by channel, rather than for full-funnel ROI. When conversions occur across multiple touchpoints - search, social, and display - tracking real influence is nearly impossible. Walled gardens prioritize their own measurement models, further obscuring true incrementality and making it difficult to justify spend allocation.

For performance marketers, the result is frustration: wasted budget, duplicated spend, and little clarity on what actually drives incremental revenue.

Omnichannel vs. multichannel: definitions that matter for ROI

Multichannel = multiple touchpoints, multiple silos

Multichannel marketing means running campaigns across separate channels - email, social, display - each managed independently. Messaging is fragmented, and data rarely moves between platforms. This isolation creates duplicated spend, as the same user is targeted in multiple places with little coordination.

Channel teams optimize for their own KPIs, not for the customer. The result: rising costs, wasted impressions, and no unified view of performance.

Omnichannel = unified data, consistent experience

Omnichannel marketing synchronizes every channel and touchpoint around the customer. Unified customer data powers real-time adaptation, so messaging changes based on individual behavior.

Integration and personalization are built-in, delivering a consistent experience whether the customer interacts online, in-app, or in-store. Brands that centralize data see fewer drop-offs, higher repeat rates, and stronger lifetime value.

The overlooked channel: financial apps

Financial apps are premium real estate for reaching Gen Z and Millennial buyers - an audience that trusts their banking apps more than any social feed. Platforms like Kard offer access to over 61 million verified cardholders at challenger banks and fintechs, delivering campaigns in a fraud-free, high-intent environment. Kard is unique with this value prop compared to other platforms. This unlocks a closed-loop, omnichannel marketing opportunity - aligning incentives, messaging, and measurement across one of the most trusted consumer touchpoints.

Why financial apps outperform traditional ad networks

Fraud-free environment: every click is human

Programmatic ad networks are plagued by invalid traffic - bots that drain budgets with zero chance of conversion. Financial app environments eliminate this waste entirely. Every interaction inside a banking or fintech app is authenticated, verified through strict bank-level security. It’s virtually impossible to generate fake engagement: breaking into someone’s financial account for ad fraud is not an option.

When you run card-linked offer campaigns, you reach only real, verified users and every dollar goes to genuine buyers.

Legacy ad networks promise fraud detection, but even the most advanced filters miss sophisticated invalid traffic. In contrast, financial apps simply don’t allow it. Every click, view, and redemption is tied to a real account, ensuring your budget is spent with complete confidence and measurable impact.

- Zero bot traffic - every action is verified

- Bank-level security protects against fake accounts and fraud

- All engagement is spend-backed, never spoofed or inflated

Premium demographics & spending power

Financial app environments capture audiences that traditional ad networks rarely reach at scale. For example, Gen Z and Millennials tend to select more modern fintech and challenger banks for everyday spend, making them a high-value segment for brands focused on growth.

Engagement rates inside financial apps are different by design. Users check balances, track purchases, and manage their money daily - these are high-frequency, high-trust touchpoints. Campaigns reach cardholders when they’re already in a spending mindset, not scrolling past ads in a feed.

Performance marketers see up to 3x higher engagement rates in financial app channels versus standard social or display. For brands targeting Gen Z or Millennials, banking apps are the new premium real estate.

- Gen Z and Millennial users are overrepresented in fintech platforms

- Above-average spending power and purchase frequency

- Up to 3x higher engagement rates vs. traditional digital channels

Rewards mechanics turn ads into value exchanges

Rewards-based advertising flips the model from interruption to value exchange. Instead of pushing banners or pre-rolls, brands offer real incentives - cashback, points, or perks - embedded within the financial app experience. This aligns perfectly with user intent: rewards are delivered when and where customers are making spending decisions.

When rewards are tied to verified transactions, conversion rates climb and every redemption is measurable down to the dollar. Value exchange marketing means users opt in, not tune out. They engage because there’s a tangible benefit for them, and marketers benefit from post-purchase attribution, seeing exactly which campaigns move the needle.

- Rewards deliver 5–15% lift in incremental sales

- Incentives align with user intent for higher conversion

- Closed-loop, post-purchase attribution - every result is measurable

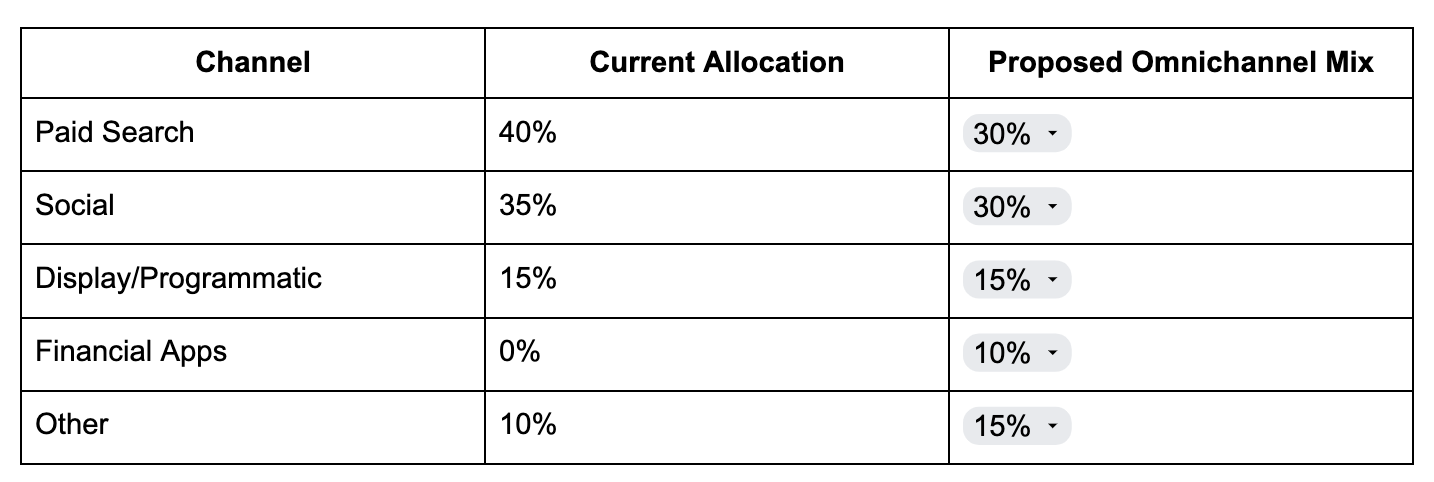

Building an omnichannel plan that includes financial apps

Budget diversification framework

Channel diversification is a risk mitigation strategy for performance marketers tired of seeing budgets eroded by CPC inflation and duplicated spend. Redirecting even a small portion of budget from over-saturated, high-CPC channels into financial apps can reveal new acquisition headroom.

A sample allocation matrix:

- Pull 10% of test budget from underperforming paid search or social

- Allocate directly to card-linked placements in financial apps

- Monitor engagement, incremental sales, and ROAS week-over-week

- Re-allocate more budget based on verified purchase data, not just impressions

This approach lets teams test new channels without disrupting core performance. Financial app placements - powered by first-party transaction data - add a fraud-free, high-intent audience to the mix. Early pilots show that reallocation consistently improves CAC efficiency and delivers clearer attribution than legacy networks.

Gradual scaling - driven by real performance metrics - lets marketers de-risk their media mix and unlock new returns without betting the farm.

Data integration & measurement

Performance marketers know that what isn’t measured can’t be optimized. Integrating financial apps into an omnichannel mix demands secure, API-driven data flows that protect privacy while unlocking full-funnel attribution.

- Integrate financial app partners via secure, privacy-compliant APIs

- Set up conversion tracking tied to verified card transactions - not just clicks

- Enable cross-channel attribution to follow the customer journey from offer exposure to purchase

- Use cohort-level reporting to measure incremental lift and optimize creative

A closed-loop setup means every dollar spent can be mapped to a real transaction, not a modeled guess. This is the foundation for ROAS clarity and campaign optimization. Marketers moving to omnichannel with financial apps should prioritize partners offering real-time, post-purchase data.

Only work with platforms that can prove GDPR/CCPA alignment and support anonymized, secure reporting. For more detail, reference the “How to get started with card-linked offers” guide.

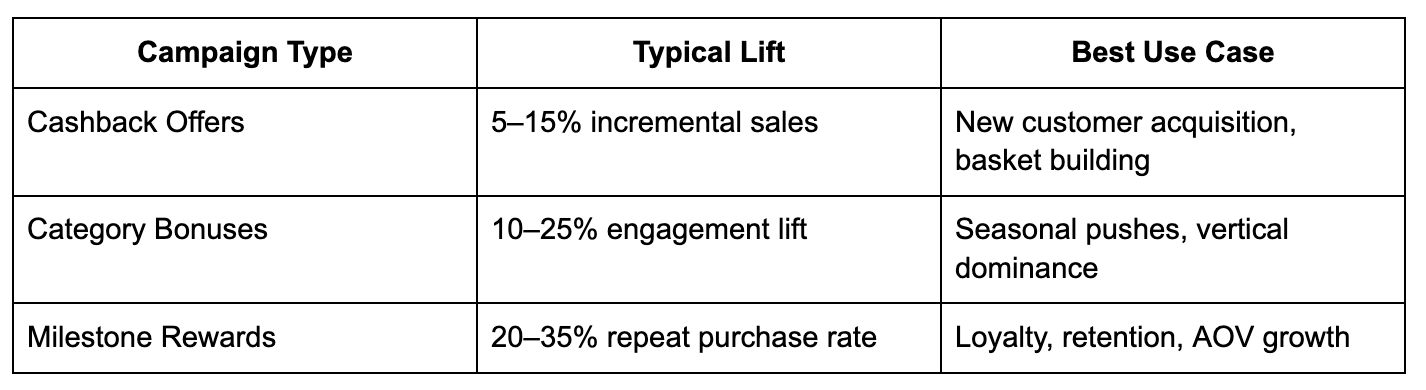

High-Performance Campaign Types in Finance Apps

Financial app campaigns outperform banners and programmatic by delivering value (not interruptions). The top campaign types for performance ROI:

- Cashback offers: Deliver 5–15% back on purchase, proven to drive both trial and repeat spend

- Category bonuses: Boost engagement in key verticals (e.g., grocery, QSR, apparel) with seasonal or product-specific incentives

- Milestone rewards: Set spend thresholds or frequency targets (e.g., “Spend $50, get $10 back”) to lift average order value and retention

Performance benchmarks:

Campaigns that align incentives with real spend - not impressions - are what drive measurable, repeatable growth in omnichannel plans.

Measuring success: KPIs that matter in financial-app advertising

Beyond CTR: focus on lifetime value

Click-through rates and impression counts have defined digital ad reporting for years, but these traditional metrics fail to capture what matters in rewards-based financial app campaigns: incremental revenue and customer lifetime value. CTR can be inflated by curiosity or bots, while impressions only measure exposure. These vanity numbers lead to misallocated spend and false confidence in channel efficiency.

A high-impact financial app campaign demands a shift to LTV-centric analysis. Start by segmenting customers into cohorts based on acquisition source, offer type, and redemption behavior. Calculate LTV for each group by tracking post-reward purchase frequency, average transaction size, and churn rate over a defined period, like 90 or 180 days. This cohort-based lens exposes which campaigns drive long-term value, not just one-time spikes.

- Traditional metrics: CTR, impressions, viewability - fail to reveal incremental revenue

- Modern LTV calculation: Track all purchases post-reward, not just initial redemption

- Cohort analysis: Identify which segments deliver repeat revenue and higher profit

Attribution models for rewards-based campaigns

Performance marketers need attribution modeling built for closed-loop environments, not guesswork. Financial app advertising enables post-purchase matching using anonymized transaction data - directly linking each campaign exposure to verified spend. This eliminates the noise of modeled conversions and last-click bias.

Closed-loop attribution means every dollar can be tied to a real transaction. Use control groups to isolate true incremental lift: compare the spend behavior of users exposed to the offer against similar users who weren’t. This approach delivers clarity on campaign effectiveness and prevents over-crediting channels for conversions that would have happened anyway.

- Post-purchase matching: Connect media spend to anonymized, verified transactions

- Closed-loop reporting: ROAS and incrementality measured with real data

- Control group methodology: True lift, not modeled assumptions

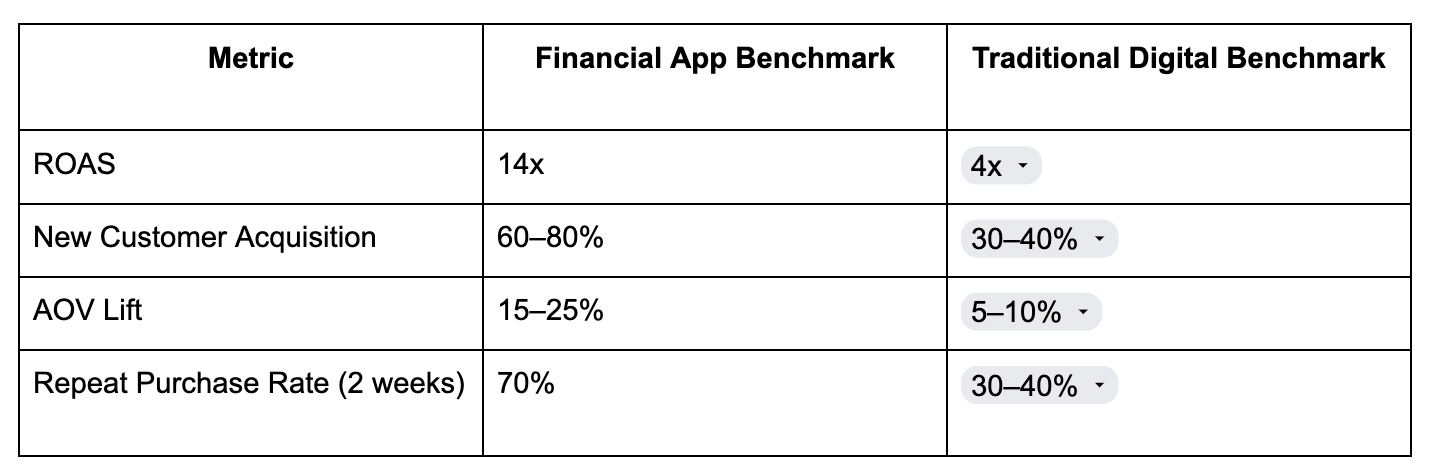

Industry benchmarks & targets

Financial-app campaigns set a new bar for ROAS and acquisition efficiency. Top-performing brands regularly achieve 14x ROAS - outpacing the 4x industry benchmark for digital campaigns. Expect new customer acquisition rates of 60–80%, especially when targeting Gen Z and Millennial segments. Average order value typically climbs 15–25% due to targeted incentives, while 70% of buyers repeat within two weeks of their first reward redemption.

These performance targets aren’t aspirational - they’re proven outcomes for brands that prioritize spend-backed, closed-loop campaigns over impression-based media.

Real-world success stories: financial app advertising results

QSR chain achieves 81% new customer acquisition

Fazoli’s moved away from legacy digital channels to focus on verified cardholder engagement inside financial apps. In weeks, they delivered $530K in sales and over 6,000 weekly redemptions. But that’s not even the real breakthrough: 81% of transactions came from truly new customers, not just serial deal hunters.

By leveraging Gen Z and Millennial targeting, Fazoli’s campaigns reached buyers when they were ready to spend, embedding offers directly in banking apps to drive closed-loop attribution that leaves no room for bot traffic or wasted impressions.

- $530K in sales attributed to rewards media

- 81% new customer acquisition rate

- 6,000+ weekly redemptions from high-intent, verified users

See the full Fazoli’s case study.

National drug store chain delivers 14x ROAS

A national drug store chain turned to financial app channels to unlock measurable, SKU-level performance improvement. By targeting both new and lapsed shoppers and activating product-specific offers, the campaign delivered a staggering 14x gross ROAS - far outperforming the 4x industry benchmark for paid digital.

SKU-level targeting enabled the retailer to push high-margin products and optimize profitability, while closed-loop reporting provided proof that every dollar spent was driving incremental transactions, not just impressions.

- 14x gross ROAS (vs. 4x digital average)

- SKU-level targeting for precise product promotion

- Profitability gains from high-intent, spend-backed shoppers

See the full drug store case study.

90-Day implementation roadmap for marketing leaders

Days 1-30: channel evaluation & budget planning

Start with a channel audit that maps to every current touchpoint, spend, and outcome. Identify where budget is leaking into duplicated impressions, inflated CPCs, or channels with weak attribution.

Fostering stakeholder alignment here is critical: bring cross-functional leaders into the process early to lock down objectives and define what success looks like.

Build a pilot budget that carves out test spend for new channels, including financial apps. Set clear, measurable KPIs tied to CAC, ROAS, and new customer acquisition. And ensure your team is trained on new attribution models, especially if moving from impression-based metrics to closed-loop spend tracking.

- Audit current channels, spend, and attribution gaps

- Align stakeholders on goals and measurable outcomes

- Define pilot budget for omnichannel and financial app placements

- Set success metrics for acquisition, ROAS, and retention

- Identify training needs for new measurement approaches

Days 31-60: pilot launch & data integration

Now it’s time to adapt your creative assets for financial app environments. Focus on offers that feel native and drive value at the point of spend. Set up API integrations with financial app partners to enable conversion tracking and real-time data flow.

Before launching your first campaign, be sure to implement a measurement framework that captures spend, redemptions, incremental sales, and retention. Use a weekly optimization cadence to review early data and troubleshoot integration issues, ensuring every impression and transaction is tied back to campaign spend.

- Adapt creative for financial app and omnichannel use

- Complete API integration for transaction data and attribution

- Deploy measurement framework: track spend, conversions, retention

- Launch pilot campaigns and monitor in real time

- Establish weekly review and optimization cycles

Days 61-90: optimization & scale

Analyze pilot results with a focus on verified transactions, incremental revenue, and cohort LTV. Refine audience segmentation to isolate high-ROAS groups and identify underperformers. Shift budget toward campaigns and channels proving out lower CAC and higher retention - and kill what isn’t working.

Optimize creative and offers based on real purchase data, and double down on high-intent placements and proven incentives. Finally, start laying groundwork for long-term omnichannel strategy: lock in integrations, build out reporting, and create a repeatable process for ongoing media budget optimization.

Analyze campaign data for ROAS, CAC, and LTV

- Refine audience segments using spend and retention insights

- Reallocate budget to top-performing placements

- Scale successful campaigns and optimize creative/offers

- Build long-term process for omnichannel strategy and reporting

The future of omnichannel: privacy, super-apps & regulation

Privacy shifts accelerate first-party strategies

Marketers are recalibrating for a privacy-first world. With GDPR and CCPA setting the standard, the ad industry is shifting from third-party cookies to authenticated, first-party data environments. Cookie deprecation is accelerating, forcing marketers to move now or lose multi-touch visibility for good.

Authenticated environments - like financial apps - are “regulation-ready” by design. Every interaction is backed by user consent and bank-level security, eliminating the guesswork (and legal risk) of tracking users across the open web. First-party data also delivers more than privacy. It enables real-time personalization, precise targeting, and closed-loop attribution - all essential for performance marketers who need clear ROI. As privacy legislation expands, only channels with built-in authentication and explicit consent will retain the signal quality brands need to compete.

- GDPR, CCPA compliance through secure user authentication

- Zero reliance on third-party cookies or fingerprinting

- Every conversion is traceable to real, opted-in users

Gen Z commerce behaviors reshape channel mix

Gen Z is rewriting the rules on commerce and channel mix. Their buying journey is mobile-first, seamlessly blending social feeds, banking tools, and rewards in a single digital flow. Users expect to manage their finances, discover offers, and complete transactions without toggling between platforms.

This convergence is driving commerce evolution — social, banking, and rewards ecosystems are merging into unified environments, where card-linked offers and embedded incentives become the new norm. Gen Z’s preference for integrated, real-time experiences forces brands to rethink how - and where - they engage.

Performance marketers who align with these behaviors win access to high-intent audiences where purchase decisions actually happen. Omnichannel strategies built for super-apps capture attention, drive conversions, and deliver measurable ROI by meeting Gen Z in the environments they trust and use daily.

- Super-apps blend social, financial, and rewards into one platform

- Mobile-first engagement is the baseline, not the exception

- Gen Z prefers real-time, integrated experiences over siloed touchpoints

Final words

Performance marketers are moving fast to patch budget leaks caused by bot traffic, rising CPCs, and walled garden attribution.

The shift from fragmented multichannel campaigns to a unified omnichannel strategy - one that taps into authenticated financial apps - delivers measurable value and scalable results.

And the merchants who adopt omnichannel marketing gain the edge - higher retention, better spend efficiency, and transparent, bot-free performance.

With financial apps playing a central role, the future is measurable, fraud-free, and built for growth.