Performance marketers are stuck. CPCs show no signs of dropping, and digitally native consumers are actively dodging traditional ads, scrolling past or blocking them entirely. And last-click attribution is breaking down as third-party cookies disappear.

In short, the channels that used to work are getting more expensive and less measurable at the same time. Card-linked offers (CLOs) are a way out of that bind.

A card-linked offer is a merchant-funded reward that surfaces inside a consumer's banking or wallet app. Some CLO platforms require users to “activate” that card-linked offer before they make a purchase.

Other CLO platforms, like Kard, complement how people shop today. With 85% of Gen Z and 82% of Millennials preferring contactless payments, Kard's frictionless CLO model automatically cross-checks every purchase for reward eligibility in the background. Consumers just tap their card and immediately earn cash back at their favorite brands. No activation step, coupon to clip, or code to remember.

The offer reaches consumers when they're already in a spending mindset, inside an authenticated environment they trust, and the merchant only pays when a real transaction happens. No wasted ad campaigns in interruptive formats, just gentle nudges to earn cash back.

In this guide, we break down what CLOs are, how they work, how they're measured, what they cost, and how to launch your first campaign without making the four mistakes that sink most first attempts.

What Are Card-Linked Offers?

A card-linked offer is a merchant-funded reward that appears in a consumer's banking, wallet, or rewards app and is tied to a specific credit or debit card. When the consumer pays with that card at the participating merchant (sometimes after activating the offer in-app, sometimes automatically), the reward is credited to their account a few business days after the transaction clears.

Some CLOs require a click-to-activate step. Chase Offers and Amex Offers work this way: the cardholder has to add the offer to their card before shopping.

Other platforms, including Kard, match the transaction to the offer automatically with no activation required, ultimately increasing redemption and engagement rates.

From day one, Kard’s API-first approach has empowered its customers to shape the consumer experience, with full control over how rewards are presented, triggered, and personalized.

Fintech marketers can accelerate brand growth, boost engagement, and push their cards to top of wallet — all without unnecessary overhead. At the same time, brands gain access to customizable notifications, gamified offers, and clear attribution.

Plus, Kard’s use of machine learning also allows for real-time offer optimization, adjusting visibility, spend caps, and targeting parameters on the fly to maximize campaign performance.

Read more about our newest product updates here.

How CLOs Work

- The merchant funds an offer with a CLO platform and defines the parameters: target audience, geography, spend cap, offer level, start and end dates.

- The offer surfaces in the consumer's banking or rewards app, either auto-applied to enrolled cards or available to click-to-activate, depending on the platform.

- The consumer transacts at the merchant using the linked card, online or in-store.

- The CLO platform receives the transaction event from the issuer network, matches it to the active offer, and confirms eligibility against the MCC code, amount, and timing.

- The reward is credited to the cardholder within 3 to 10 business days. The merchant gets invoiced (usually monthly) only for transactions that qualify.

The CLO platform takes a margin on the funded offer, and the distribution partner (neobank, traditional financial institution, fintech) takes a revenue share in exchange for placing the offer in front of their cardholders.

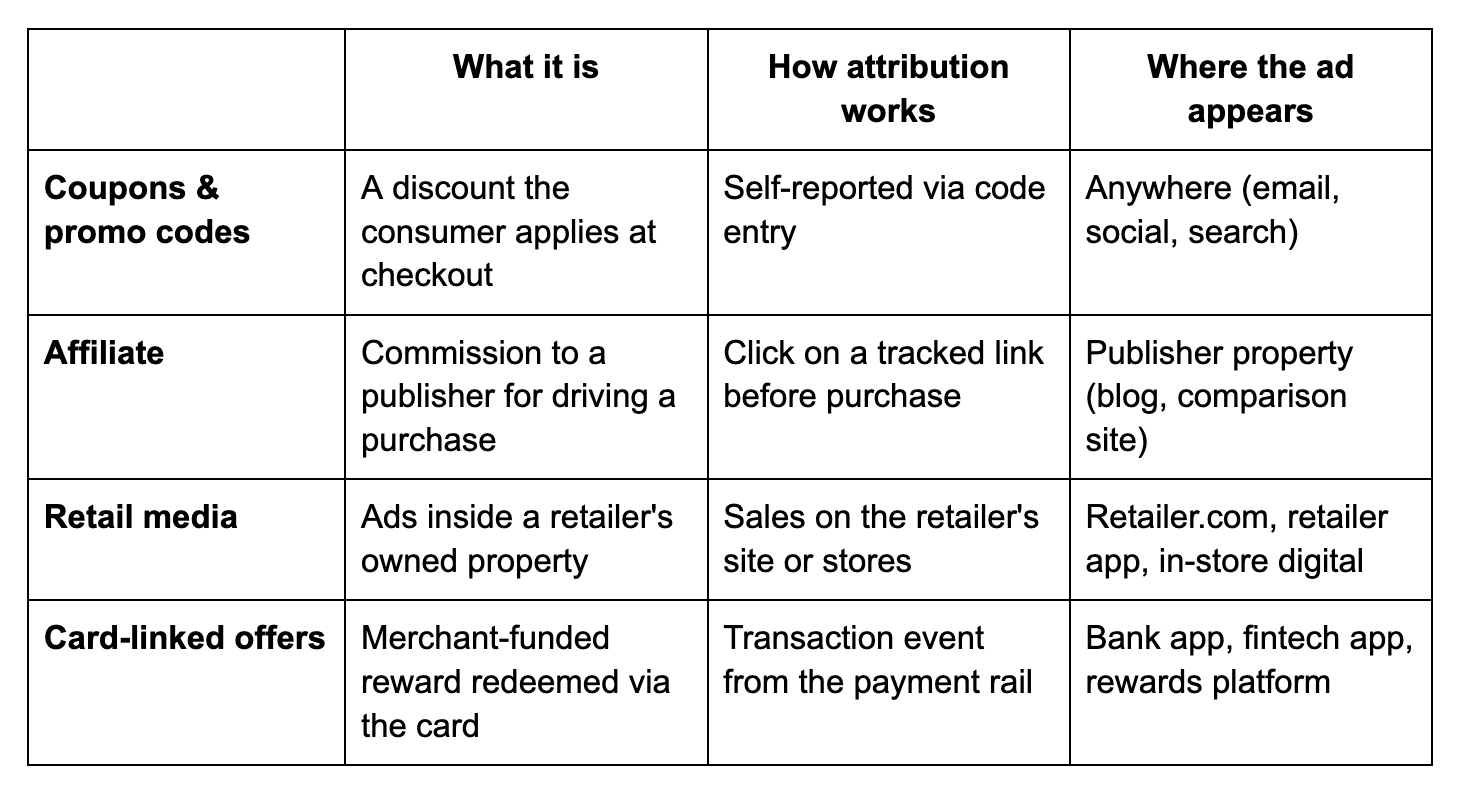

Card-Linked Offers vs. Coupons, Affiliate, and Retail Media

CLOs get confused with three adjacent channels. Here's the difference:

The biggest functional difference: CLOs require no click and no code. The card itself is the attribution mechanism. That makes CLOs the only channel that cleanly closes the loop between digital exposure and offline purchase.

Why Card-Linked Offers Matter in 2026

Three forces converged this year that pushed CLOs from a side bet to a budget line.

First, banks have become daily-use apps. People check their balance more often than they check Instagram. That's an authenticated, high-attention surface with no equivalent on the open web.

Second, performance marketing budgets are tightening. CFOs want proof that ad spend produced a transaction, not an impression. CLOs are one of the few channels where the bill arrives only after the purchase happens.

Third, deterministic identity on the open web is collapsing. Chrome's third-party cookie sunset, Apple's ATT, and the slow death of last-click attribution have made first-party transaction data one of the few signals left standing.

And then, there’s the rise of commerce media.

Commerce media (the practice of brands buying ad placements inside platforms that also process the transaction) is the fastest-growing category in advertising. WPP forecasts it will account for nearly a fifth of total ad revenue by 2030.

Card-linked offers are the engine that makes commerce media work for banks. Retail media networks like Amazon Ads or Walmart Connect can close the loop because the same company shows the ad and rings up the sale. Banks couldn't do that until CLOs came along. Now they can: the bank app shows the offer, the linked card confirms the purchase at any merchant, and the transaction data ties exposure to redemption without a cookie, a click, or a self-reported code.

That's why every major payment network is now in this market. Mastercard launched its commerce media offering in October 2025. Visa and the major issuers are following. If you're building a commerce media plan in 2026, CLOs are the line item that connects bank-app inventory to actual revenue. For more on how this fits together, see our commerce media strategies guide.

6 Benefits of Card-Linked Offers for Performance Marketers

Because card-linked offers integrate directly into consumers’ banking apps or credit card rewards platforms, they have a significant edge over traditional ads in terms of:

1. Not Feeling Like an Ad

Unlike pop-ups or display ads, card-linked offers don’t show up on a recipe or random news story.

They’re displayed in a highly secure, authenticated environment: banking apps. Consumers see card-linked offers when they go to the rewards section of their banking app, creating an experience that feels intentional rather than intrusive, maximizing attention and driving higher engagement.

Plus, consumers associate financial institutions with trustworthiness and protection, and tend to extend that trust to card-linked offers.

In fact, in their minds, cash back offers seem more like a coupon. Whenever they have to make a similar purchase, they’ll remember the cash back and great product they got, and likely shop at the same retailer, driving loyalty with the brand and cardholder spend.

2. Brand Safety

Even if you pay the big bucks, programmatic ads can appear on content that’s not aligned with your brand’s values. Every time that happens, your reputation takes a hit.

With a CLO platform, you never have to worry about where your ad is placed. It’s always going to show up in people’s banking apps.

Even better, the rewards listed next to your offer have been hand-selected by the issuer, ensuring that they are legitimate. Depending on what CLO network you go with, showing up alongside those other brands’ offers could give your brand reputation a boost.

3. Right-Time Targeting

Card-linked offers promote your brand to people already in a money mindset.

“Consumers are in their banking app because they’re thinking about spending money and trying to get a deal. If your brand pops up there, they associate you with something worthwhile to spend money on,” Blake Ziolkowski, Kard’s Senior Director of Merchant Sales and Operations, explains.

With some platforms, like Kard, you can get even more granular with who you’re targeting and adjust your offers accordingly. For example, you might give consumers a diminishing discount structure:

- Get 15% off on a first purchase

- Get 10% off on a second purchase

- Get 5% on the third purchase

A continuous rewards cycle shows your customers you care about their loyalty, which improves retention and LTV. In our experience, this framework often leads to higher average order values as well.

4. Free Impressions

Some CLO platforms, like Kard, only charge when a consumer uses an offer. Potential customers could be looking at your offer in their banking app every day, nudging them closer and closer to making a purchase. And you wouldn’t have to pay for any of those impressions.

And once the consumer does make a purchase, brands potentially gain a new customer for life.

5. Personalized Engagement

CLO platforms like Kard collect impressions and view events, tracking whenever users engage with rewards experience touchpoints. This data clues issuers and brands into:

- What offer messaging works best

- What offer presentation drives clicks

- What kinds of offers produce the most engagement

With these datapoints in mind, issuers and brands can develop more personalized offers that drive engagement and loyalty.

At Kard, we are collecting all the transaction data, so can tell you what other stores your ICP shops at and other spending habits they have, helping inform not only additional CLO campaigns, but other marketing campaigns you may want to run in the future.

6. Zero Fraud

Ad fraud is a persistent challenge in digital marketing. A study by Juniper Research found that 27% of organic and direct traffic consists of bots and fake users. And by 2028, $170 billion in ad spend will be lost to ad fraud.

With CLOs, you don’t have to worry about bots eating up your ad budget.

For CLO fraud to happen, a hacker would have to steal someone’s phone, log into their banking app to see what rewards they have, use the proper card to make a purchase, and somehow route the cashback back to them. The chances of that happening are extremely low.

Every interaction with a CLO campaign represents genuine consumer engagement — a great thing when you consider that some CLO platforms only pay for performance.

Card-Linked Offer Measurement

To get ongoing budget for rewards, brand and loyalty marketers need to be able to answer a crucial question: did our offers actually influence purchasing behavior, or did it simply reward actions that would likely have happened anyway?

At Kard, we do this by measuring incrementality:

- Create statistically equivalent groups: Divide your audience into test (80%), control (10%), and reserve (10%) segments

- Expose only the test group to your offers: The control group receives no marketing intervention

- Measure the difference in outcomes: Compare key metrics between groups to reveal the true incremental impact

This approach allows you to measure meaningful business outcomes like conversion rates, spend rates, average order values, and transaction frequency while controlling for all other variables.

5 Other CLO KPIs to Track

- Incremental ROAS. Revenue from incremental purchases divided by total CLO spend (funded offers plus fees). Let’s say your CLO campaign generated $500K in incremental sales (above what the control group spent) on $100K of total program cost. Your incremental ROAS would be 5x.

- New-to-brand redemption rate. The share of redemptions from cardholders who haven't transacted with you in the last 12 months.

- Average order value lift. The percentage difference in average basket size between exposed and held-out audiences.

- Redemption rate per impression. The percentage of cardholders who see your offer and then make a qualifying purchase.

- Repeat purchase rate among redeemers. The share of first-time redeemers who come back for a second purchase within 90 days. This separates loyal customers you've acquired from one-time deal hunters.

What Card-Linked Offers Cost

Pricing Models

Three structures cover most of the market:

- CPA / cost-per-redemption. Merchants pay a fixed fee per qualified transaction on top of the funded offer.

- Funded-offer only (pure pay-for-performance). Merchants fund the offer plus a platform margin. With Kard, for example, there's no cost to join the merchant network. You get free impressions inside banking apps, and you only pay when someone actually makes a qualifying purchase.

- Hybrid. Funded offer plus a CPA on each redemption.

The right model depends on how predictable your unit economics are. If you have tight CAC tolerances, a fixed CPA is easier to forecast. If you have margin to share and want to maximize redemption volume (and free impressions in the meantime), a funded-offer-only model usually produces more reach.

Typical Funded-Offer Ranges (By Vertical)

Industry ranges, with the obvious caveat that your exact rate depends on platform, audience, and category competition:

- QSR and restaurants: 5 to 15% cashback

- Retail and apparel: 5 to 10% cashback

- Subscription and SaaS: Often flat-dollar (e.g., $5 back on a $30+ purchase)

- Travel: Up to 20% on larger baskets

- Grocery: 2 to 5%, but with higher repeat rates

Want to learn more about how consumers spend in each category? Download our 2026 Consumer Research Report.

What’s Negotiable

Spend caps, exclusivity (whether your offer competes with other brands in the same category on the same network), audience targeting depth, and reporting cadence are negotiable on most platforms. Platform take rates and margins are usually fixed unless you're spending at top-tier levels.

Results From Real CLO Campaigns

The case study below is the cleanest CLO acquisition story we've published. The benchmarks that follow are industry-typical ranges, not Kard-specific.

Case study: Fazoli's drives 81% new customers

Fazoli's, the fast-casual Italian chain, came to Kard with three problems. Acquiring younger, digital-first customers was getting harder. They had few levers to push average order value. And they wanted to reactivate lapsed guests without offering blanket discounts.

Working with Kard, Fazoli's launched a 4% cashback offer targeted to a tech-savvy demographic identified through transaction data. The campaign brought in:

- $530K+ in sales

- 6,000 offer redemptions per week

- 81% of redemptions from people who had never eaten at Fazoli's before

New-to-brand rates above 60% are strong. Above 80% is exceptional, and it's the kind of acquisition cost story that's nearly impossible to produce on Meta or Google for a regional QSR.

What “Good” Looks Like

Rough benchmarks based on industry-reported ranges:

- QSR: 60 to 80% new-to-brand on well-targeted campaigns

- Retail and apparel: 3 to 6x incremental ROAS at scale

- Subscription: First-month retention lift matters more than ROAS

- Grocery: Repeat rate and basket size lift are the primary metrics, not new-to-brand

If your platform isn't producing numbers in these ranges after a properly run test, the issue is usually offer level, audience definition, or issuer footprint, not the channel.

How to Launch Your First Card-Linked Offer Campaign

Step 1: Define Your Audience and Goal

The four most common CLO goals are new customer acquisition, lapsed reactivation, AOV lift, and category-switcher acquisition (stealing from a competitor).

Pick one to focus on at first. Campaigns trying to do all four at once produce muddy results and hard-to-defend ROAS numbers.

Step 2: Choose Your Offer Structure

Think about:

- Flat dollar vs. percentage cash back

- One-time versus diminishing (15% on first purchase, 10% on second, 5% on third) versus tiered by spend ($5 off $30, $10 off $60)

Diminishing structures pull AOV up because they reward larger baskets. Flat structures are easier to compare against other channels because the unit economics are cleaner.

Step 3: Pick a Platform

Five things to evaluate, with a note on whether the responsibility sits on the merchant side or the issuer side:

- Issuer footprint (issuer-side). Does the bank network actually reach your target audience? The platform's issuer relationships determine which cardholders see your offers. Ask for the demographic and geographic breakdown of the cardholder base before you sign.

- Targeting depth (merchant-side). Can you build audiences from transaction history, like cardholders who shopped a named competitor in the last 90 days, lapsed customers from the last 12 months, or specific spend tiers? Shallow targeting (just geography and broad category) limits what the channel can do.

- Customization (shared). Can you control the look, the notification timing, and the offer logic? Issuers want creative consistency with their app; merchants want the offer to reflect their brand. The platform sits in the middle and either enables that flexibility or doesn't.

- Attribution rigor (merchant-side). Can the platform run a true incrementality test with a held-out control group, or does it only report gross redemptions? If a vendor can't prove that your offers caused incremental purchases, you can't defend the spend internally.

- Pricing model (merchant-side). Pay-for-performance models charge only when a redemption happens, so you get free impressions while consumers consider. CPA and hybrid models charge per redemption on top of the funded offer. Pick the structure that matches your unit economics and your finance team's tolerance for variable spend.

Step 4: Set Up Measurement Before You Launch

Ask your platform provider how they prove that your offers actually contributed to a purchase. Specifically: can they show you the holdout group, the pre-period spend matching between groups, and the methodology used to calculate incremental lift?

Decide upfront which KPIs you'll report to your finance team and which thresholds count as success. The worst version of this conversation is the one that happens three months in, when results are already rolling in and there's no shared definition of "working."

Step 5: Optimize Your Offers

Most modern platforms allow real-time changes to caps, audience, and offer level.

Plan for at least one mid-campaign adjustment based on early redemption data. If redemption is below benchmark in week two, the lever is usually offer level or audience expansion, in that order.

4 Common Pitfalls

Four mistakes account for most failed CLO programs.

- Treating CLO as one part of the funnel. A common mistake is targeting only existing customers (subsidizing purchases they'd make anyway) or only new customers (missing easy lift from your highest-value cohorts). The strongest programs run offers across all three: new customers for acquisition, lapsed customers for reactivation, and existing customers for AOV lift and repeat purchase rate.

- Skipping the incrementality test. Then spending the next quarter arguing internally about whether the channel worked. Know ahead of time how you’re going to prove that you’re getting ROI from your rewards.

- Picking a platform with the wrong issuer footprint. A Gen Z DTC brand on a platform whose users skew toward traditional banks with older cardholders will produce disappointing results no matter how good the targeting tools are. Ask for the demographic breakdown of the cardholder base before signing.

- Forgetting to set spend caps. A high-performing offer can scale faster than you expected. Cap the budget at the campaign level and the daily level to get the invoice surprise out of the way before it happens.

The Future of Card-Linked Offers

Here’s What’s Happening Now

Beyond SKU-level targeting (rewarding a specific product, not a brand) and multi-merchant ecosystems where a single journey triggers rewards from multiple brands, we’re seeing:

Rewards That Encourage Repeat Purchases

The more a user engages with a brand, the better they expect their rewards to get. That’s why we’re seeing a rise in:

- Purchase count offers: A user receives a reward after a specific number of purchases from a brand within a given timeframe — think of it as a punch card.

- Spend-tiered offers: A user receives a reward if they spend a specific amount (or more) with a brand.

- Tap-to-renew offers: After making a purchase and receiving a reward, a user can extend the offer to their next purchase, leading to more card activity for the issuer and repeat business for the brand.

Rewards That Create Urgency

Scarcity closes the gap between passive interest and an actual purchase. Which is why we’re seeing offers that give users a reason to act right now:

- “Flash” offers: A user can only redeem it during a certain period of time.

- “While supplies last” offers: A user can only redeem an offer while it’s still available. Once a set number of users have redeemed an offer, it closes.

Here’s What We Predict Will Happen Further Out

Gamified formats like click-to-boost and progression milestones will become all the rage, as will event-driven push and email notifications tied to offer redemption windows.

You might even see mobile wallet-native CLOs that surface directly in Apple Pay and Google Wallet rather than inside a separate bank app.

Eventually, you may even see cross-brand collaborative loyalty programs where multiple brands pool audiences and rewards. This model requires the most coordination between issuers and merchants (why it's slower to arrive).

Bought into CLO, just not sure which platform to go with? Here are six questions to ask in your evaluation.

If you're ready to see what a true pay-for-performance CLO platform looks like, we can help.

Kard is a rewards infrastructure platform with 47M+ users across our issuer network and visibility into $31B+ in annual transactions. We work with brands across QSR, retail, subscription, and grocery to run incrementality-tested, pay-for-performance CLO campaigns through banking, fintech, and rewards apps.

Want to see what our CLO platform can do? Book a demo today.

Frequently Asked Questions About Card-Linked Offers

What is a Card-Linked Offer?

A card-linked offer is a merchant-funded reward that appears in a consumer's banking, wallet, or rewards app and is tied to a specific credit or debit card. When the consumer pays with that card at the participating merchant (sometimes after activating the offer in-app, sometimes automatically), the reward is credited to their account a few business days after the transaction clears.

How Are Card-Linked Offers Measured?

Through incrementality testing. A random subset of the targetable audience is held out from seeing the offer, and the spend difference between the exposed and held-out groups is the incremental lift. Last-click attribution systematically undercounts CLOs because most redemptions never involve a click.

Are Card-Linked Offers Privacy-Compliant?

The best platforms don't collect personally identifiable information and operate under SOC 2 and PCI compliance standards. The targeting signal is anonymized transaction data, not personal identity.

Which Industries Use Card-Linked Offers?

Restaurants, retail, grocery, travel, and subscription services account for most current CLO spend, but the channel is expanding into auto, telecom, and streaming.