Gen Z has $450B in spending power. Let that sink in.

Then consider that that number is growing every year — more and more of Gen Z will start entering the workforce. And by 2030, NielsenIQ projects they will be the highest-spending generation in history, reaching $12.6 trillion in total spend.

If you can get them interested in your product and grow them into big fans now, you’ll be sitting really pretty later. The challenge is that most of what marketers know about this generation comes from surveys — which tell you what Gen Z says they value, not how they spend their money.

Transaction data tells you exactly how they behave. And we have it: over the past two years, we’ve analyzed billions of transactions to mine the patterns of young consumers.

Below, we share what our data shows — alongside what other research has found — so brands and distribution partners need to design rewards programs that reel Gen Z in and keep them coming back for more.

Gen Z Is Already a Card-First Generation

Over 25% of Gen Z adults between 18 and 29 with a FICO Score opened at least one credit card in the past year: the highest rate of any age group. EY’s Future Consumer Index reports that 69% use debit cards daily or weekly.

For brands, that means Gen Z is transacting on card rails constantly. Every grocery run, every QSR order runs through a card or linked payment.

For issuers, the window to establish a primary card relationship is open now. Gen Z is actively building financial habits, and those tend to be sticky over time.

Where Gen Z Spends

The highest-frequency categories

In Kard’s 2025 dataset, big box retail — Amazon, Target, Walmart — accounted for 23% of total cardholder spend, outpacing the next highest categories by 13%+. QSR came in at 10%, gas and convenience at 10%, and grocery at 8%.

Gen Z visits these categories weekly, sometimes more.

For brands in these verticals, the volume is there. The question is whether your offer is present when Gen Z is already spending in your category (otherwise, that spend goes to a competitor).

For issuers, a rewards program tied to what cardholders actually buy weekly gives them a concrete reason to use the card rather than a competitor's.

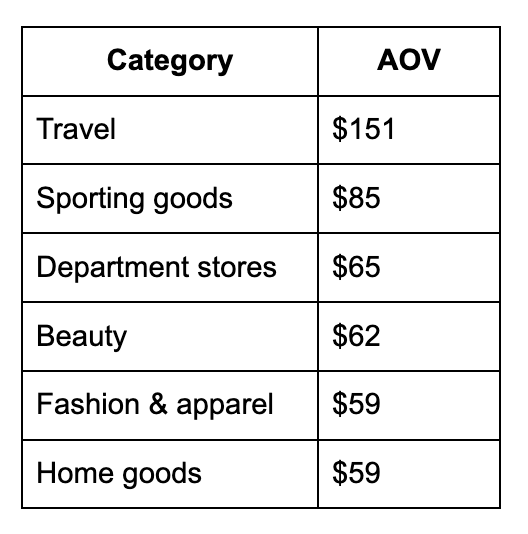

The highest AOV categories

Wallet share tells you where Gen Z shops most, but average order value tells you where they splurge. In discretionary categories, that gap is significant.

The average AOV across all verticals is $27, but travel runs at 459% above that. Even fashion and home goods are more than double the average AOV.

McKinsey found that 65% of Gen Z say they're willing to splurge in categories that matter to them, and that Gen Z ranked as the highest-spending generation in every country they surveyed (18 total).

For brands in high-AOV categories, a cash back offer can be what tips a $59 fashion purchase or an $85 sporting goods order from just sitting in someone’s cart to showing up at their doorstep.

For issuers, these are the transactions where cardholders decide which card to reach for, and if yours gives them higher rewards, you’re getting their engagement.

How Gen Z Pays

In Kard's 2025 dataset, financial services, gas and convenience, and grocery collectively represent 18% of total spend — driven primarily by debit, credit, and EBT card transactions. (Kard, 2025 Consumer Trends in Retail) Gen Z reaches for their card for everyday necessities by default.

Alternative payment methods are growing fast alongside that.

The financial services category grew from 9% of spend in March to 12% in December — a 33% increase over the course of the year. PYMNTS found that nearly 1 in 5 Gen Z use BNPL alongside other pay-later methods (compared to 12% of older consumers).

36% of 18 to 24-year-olds say they would choose a fintech over a traditional bank for online payments.

For brands, this means Gen Z pays across more surfaces than other generations. To capture their dollars, you need to be present on all of them.

For issuers, Gen Z is actively spreading their financial activity across multiple apps and providers. Make sure you’re offering the most relevant experience and rewards.

Being stored is being used

45% of online shoppers used stored merchant credentials for their most recent purchase.

For brands, if you're not where Gen Z checks out by default, you lose the transaction to whoever is.

For issuers, a card that isn't stored at the merchants Gen Z uses most won't get used.

The Rewards Gap

IPSOS found that 70% of Americans prefer to pay by card to earn rewards or points, and 65% have opened a credit card specifically for the rewards. 61% of rewards cardholders redeemed rewards for cash back or gift cards in the past year.

So, why aren’t your rewards getting the attention and engagement they deserve? The problem might be a category mismatch.

Travel rewards and dining perks make sense for a cardholder who flies frequently. For a 24-year-old whose top spend categories are big box, QSR, gas, and the occasional sporting goods splurge, those rewards don’t mean that much.

Cash back and other forms of rewards need to be tied to what they're already buying.

Kard's 2025 transaction data shows Gen Z's spend is concentrated in high-frequency essentials and selective high-ticket discretionary purchases. QSR has one of the lowest AOVs in Kard's dataset but the fourth-highest vertical share — Gen Z visits these merchants constantly, out of routine.

As Kard's CEO, Ben McKinnon, puts it:

"It's hard to change buying behavior. Most consumers stick to familiar patterns: the same lunch spot, the same skincare brand, the same pet store. With rewards-based offers you don't need to change those habits — you can just shift them from your competitors to your brand instead."

Did you know? Kard's merchant-funded rewards network connects both sides — brands reach Gen Z cardholders through the banking apps and fintech platforms they already use daily, while issuers offer differentiated rewards without funding them from their own margin.

More on how issuers are building this into their programs here.

When to Reach Them

In our dataset, average daily spending was 27% higher on weekdays than weekends. Gen Z and Millennial consumers — many of whom work from home or carry flexible schedules — do more of their spending during the week than most marketers assume, particularly on essential categories such as grocery, gas, and quick-service restaurants.

The categories that bucked trend this were:

- Department stores (+17% weekend lift)

- Beauty (+17%)

- Home goods (+12%)

- Fashion and apparel (+9%)

- Full-service restaurants (+8%)

- Sporting goods (+7%)

While specialty and apparel brands might benefit from weekend cash back offers and other marketing campaigns, most other brands would do better with Sunday or Monday promos to encourage spend throughout the week.

For issuers, in-app engagement and offer surfacing should follow this logic, too.

The Window Is Now

62% of fintechs are already developing products with Gen Z in mind. Competition for their attention — from both the FI/fintech and brand side — is getting more and more crowded.

Gen Z already holds multiple cards, uses fintech alternatives, and switches brands more readily than any prior generation. And the traditional advantages (that switching banks is a hassle, that a familiar brand name carries loyalty) are weaker with this cohort than any before it.

To really stand out, brands are going to have to adjust their marketing strategies and think outside the box to meet Gen Z where they are, and issuers are going to have to match their rewards to how Gen Z spends, not how older cardholders do.

Kard can help with both.

Learn more about how thoughtfully cash back offer campaigns acquire, engage, and retain Gen Z customers. Book a demo with one of our experts today.