Every neobank offers the same combo of perks to get you to sign up.

- No monthly fee

- Early direct deposit

- A referral payout

- Decent savings rate

Exceptional rewards would set them apart. Who wouldn’t want cash back on something they were already going to buy?

The problem is that rewards seem expensive, especially for a neobank running on thin interchange margins. But there is a way to compete: getting merchants to pay.

Instead of funding cash back out of your own budget, you connect your cardholders to brands who are willing to pay a pretty penny to reach them.

Cardholders spend at a participating merchant → the merchant covers the reward → you take a cut for providing the distribution channel: your app, your card, your cardholder base.

Below, we cover why rewards can be a primary growth lever for neobanks, the kinds of rewards that appeal to neobank users, and how to prove a merchant-funded rewards program works.

Why neobanks need rewards

You’re far from the only neobank cardholders have to choose from. And if you’re offering the same rates, the same fees, and the same everything as everybody else, it’s going to be really hard to attract new customers, let alone retain them.

Rewards are one of the few places left to stand out, and they work.

80% of consumers say they value rewards, and roughly 70% of rewards cardholders prefer to pay with a rewards card because of its benefits. The card people reach for is the card with the better reward.

Here’s what rewards can do for a neobank, specifically.

Boost Acquisition

A rewards program is a hook at the top of the funnel. People want to earn rewards at the places they already shop — the grocery store they go to every week, the gas station on their commute, the coffee spot they stroll into on slow Sunday mornings.

When your card pays them back for spending they're going to do anyway, signing up is an easy yes. It feels like they’re going to see value right away.

Rewards on debit spend also reach the exact customer neobanks want. Debit is the most-used payment method for Gen Z, with 69% using it daily or weekly, per EY. A reward attached to everyday card use lands right where this audience already pays.

Increase Retention

No neobank wants to be some side account a cardholder opened on a whim a few months ago. The goal here is primacy, to be the account a customer routes their paycheck and daily spend through.

The card that pays them back every time they swipe is the card they'll keep reaching for. Offer rewards when they set up direct deposit, when they pay bills from the account, when they use the card for everyday spend — and you give customers a real reason to make you their primary bank.

Promote Engagement

A neobank lives in an app the customer has to choose to open, and the quality of that experience now drives real card behavior.

PYMNTS found that 69% of cardholders say app quality influences which card they use most. And among Gen Z, that jumps to 87%. Nearly a third of app users say they spent more on a card after adopting its mobile app, rising to 44% for Gen Z.

The flip side is just as real, though. 24% of cardholders have cut back or stopped using a card because the app was weak, and that goes way up with Gen Z.

A fresh, relevant reward is one of the strongest reasons to come back. Every app open is a chance to surface a new offer, prompt a transaction, and stay top of wallet. Frequency builds habit.

Want to let your cardholders know about your rewards without annoying them? Read our latest guide to promoting your rewards program.

Turn Rewards Into Revenue

Paid ads, referral bonuses, and sign-up incentives all pull from your budget before they ever yield any return.

Merchant-funded rewards change the entire business case: brands are paying you to market to your customers. And because your customers are getting rewarded for shopping at stores they already frequent, it builds loyalty on both sides — they keep coming back to the brands they love, and they keep reaching for the card that pays them to do it.

The Kinds of Rewards Neobanks Need

A flat 1% on everything is easy to launch and easy to ignore. The rewards that actually move the needle share three traits.

Targeted to the Right Customer

A new cardholder, an active one, and a lapsed one all need something different.

- A welcome offer nudges a new customer toward their first swipe.

- A relevant offer keeps an active customer spending.

- A win-back offer pulls a lapsed customer back into the app.

The brands behind the offers matter just as much.

Merchant-funded rewards land when the brands funding them are ones your cardholders already like — the restaurants they eat at, the retailers they shop at, the apps they use every week. Put a brand they already love in front of the right segment, and the reward is way more likely to get used.

Timely and Urgent

A reward with no deadline carries no urgency.

Dynamic rewards like limited-time offers, event-driven prompts, and reminders tied to a customer's actual behavior are what drive action. An offer that lands the morning someone usually orders lunch beats the same offer buried three taps deep in a menu.

Visible

A single email on launch day isn’t going to cut it. Across all industries, the average email open rate hovers around 21% to 23%.

That means just 1 in 5 recipients opens a single email sent to them. To capture their attention (and keep it), your launch and ongoing rewards campaigns need to be a full-blown sequence — across channels, across time.

Rewards Without the Huge Cost

Strong rewards cost money, and neobanks run on thin margins. The way through is to stop funding the rewards yourself.

The Interchange Problem

US neobanks fund most rewards out of interchange, the small fee earned every time a customer swipes. It's a few cents on the dollar. Self-funded cashback comes straight out of that. Pay 1% cash back and you've handed away a huge share of the revenue the transaction generated.

Cashback is easy for customers to understand, but it's a high direct cost with an uncertain return.

Huge issuers like Chase and American Express can absorb rich rewards because they sit on premium interchange and balance-sheet scale. A challenger that tries to win by paying more cashback is just racing toward a negative margin.

How Merchant-Funded Rewards Work

A neobank surfaces a brand’s offer inside its app — say 5% cash back at a regional restaurant chain. The customer pays with their linked card. Once the transaction gets verified, it’s a win-win-win:

- The customer gets a reward that feels generous without having to input any codes or coupons

- The brand gets a measurable customer

- The neobank delivers real value at close to zero marginal cost (while earning revenue on top)

Let’s run the math on a single offer:

A customer spends $40 at that restaurant. The brand funds 5% cash back, so $2 goes to the customer’s account.

The neobank pays none of it and collects a commission on the verified sale. That same $40 swipe on a self-funded 1% program would have cost the neobank $0.40 out of its own interchange.

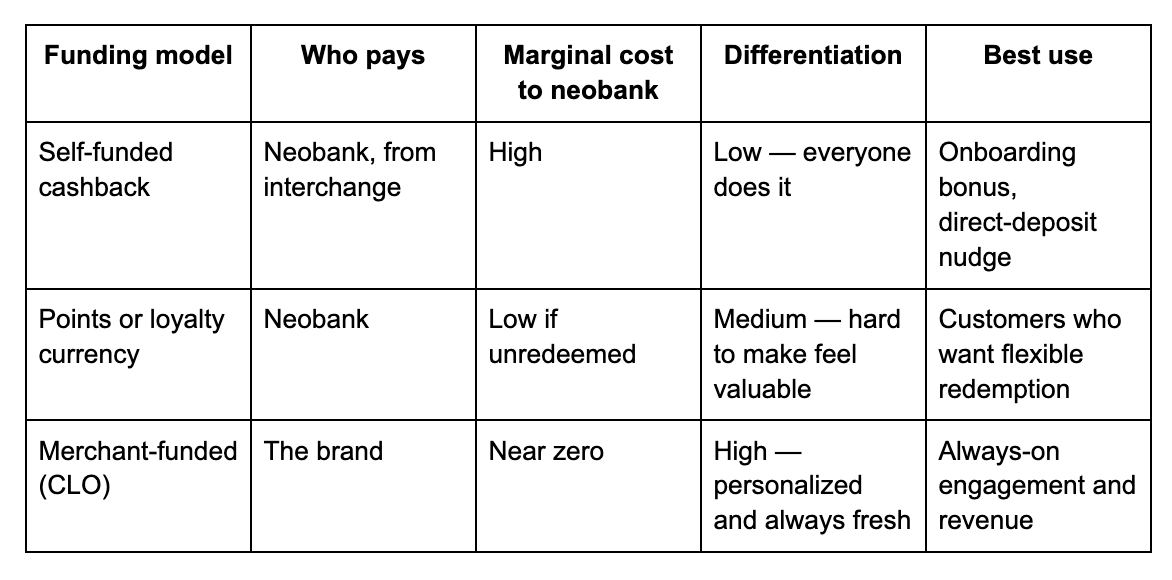

Rewards Funding Models, Side By Side

The practical play is to layer them. Use self-funded rewards sparingly, where they buy something specific like onboarding or a direct-deposit switch. Run merchant-funded offers as the always-on engine, so your payout doesn't scale against you as the program grows.

Build Rewards In-House or Plug Into a Rewards Demand Network?

Once a neobank commits to merchant-funded rewards, the next question is build or buy.

Building it yourself means signing merchants one at a time, constructing the offer engine, matching transactions, and reporting on all of it. That's months of work, it pulls engineers off your core product, and a single neobank rarely has enough merchant demand on day one to make the offers compelling.

The alternative is plugging into a network that already has the brands, the infrastructure, and the demand.

With Kard, for example, neobanks get an existing roster of merchant-funded offers and the tools to run and measure them, so a small team can stand up a rewards program that competes with the biggest banks at a fraction of the cost. The brand demand is already there, which means offers are relevant from your first launch — not after two years of business development.

And because every team builds differently, Kard offers three ways to integrate, all running on the same API backbone:

- Direct API. Maximum flexibility for teams that want full control. Our docs are structured to work with AI coding tools like Claude Code, Cursor, and Copilot.

- Server-side SDKs. A single package install in TypeScript, Python, Java, Go, or .NET replaces hundreds of lines of custom code. The front-end is still yours to design.

- Hosted WebView. A polished, themed rewards UI live in days, embedded on iOS, Android, React Native, or web. Every new offer format we ship shows up automatically.

We’ve designed these models to be complementary, so you can even mix and match. For example, you could:

- Use WebView for the rewards tab and the API or SDKs for everything else.

- Use SDKs on the backend and direct API on the frontend.

- Use the direct API and llms.txt for prototyping, and SDKs for production.

Track the Metrics That Prove It's Working

A rewards program is only as good as what it changes. Tie your metrics to the three jobs the program does.

- For acquisition, watch cost per acquired customer and referral rate. If rewards are pulling weight at the top of the funnel, CAC holds steady or drops while new accounts climb.

- For engagement, watch enrollment rate, offer redemption rate, and active users. These tell you whether customers are actually noticing the rewards and acting on them. Flat redemption usually points to a visibility problem, not a reward problem.

- For retention and primacy, watch churn among engaged versus unengaged customers, direct-deposit attach rate, and transaction frequency. Rising frequency and direct-deposit rates are the clearest signs you're becoming a primary account instead of a backup card.

Note: Be sure to measure incrementality, not raw redemptions. A redemption tells you a customer used an offer. Incrementality tells you the offer changed what they would've done anyway. Run offers against a control group so you know which rewards drive new behavior and which are just discounting spend that was already coming.

Ready to Get Your Rewards Front and Center?

Rewards are the one lever left that can actually set you apart, and merchant-funded rewards are how you pull it without blowing up your margin.

But a rewards program isn't something you set and forget. It’s something you have to keep refining and keep notifying your cardholders about. After all, the brands paying to get offers in front of customers expect their dollars to move product.

Being a neobank actually plays in your favor here. You own the app, the notification rail, the home screen. The big banks are still fighting their own legacy UX to get rewards in front of cardholders. You can put a relevant offer on the first screen a customer sees the moment they open the app and update it the next time they open it, too.

Want the full playbook on getting yours in front of cardholders — without being too in their face? Read our ultimate guide to promoting a cash back rewards program.